Demand Analysis Class 12 Practice Paper with Answers

Demand Analysis Class 12 Practice Paper with Answers

What is Demand?

- Goods are demanded because they have utility

- Demand is the quantity of a commodity that a person is ready to buy at a particular price during a given period of time.

- In economics the term ‘Demand’ refers to a desire for a commodity backed by the ability to pay and willingness to pay for it.

- Demand = desire + ability to pay + willingness to pay

Explain the Types of demand

- Direct demand: – When goods and services are demanded to satisfy human wants directly, it is called direct demand. E.g. demand for food, clothes, computer, mobile, etc.

- Indirect demand / Derived demand: – When demand for one commodity gives rise to the demand for another commodity, it’s called indirect demand. E.g. raw materials, labour, machines, etc. are not demanded to serve directly but they are needed for the production of goods having direct demand.

- Joint demand / Complementary demand: – When two or more commodities are demanded at the same time to satisfy a single want, it is called joint demand. For e.g. car and petrol, pen and paper, toothbrush and toothpaste, etc.

- Composite demand: – When one commodity is demanded for number of uses, it is called composite demand. For e.g. electricity is demanded for lighting, cooking etc. or Milk is used for making tea, coffee, ice-creams, etc.

- Competitive demand: – When two goods are close substitutes of each other or when the demand for a commodity competes with its substitutes, it’s called competitive demand. E.g. tea or coffee, Pepsi or cola, etc.

What are the Determinants of demands/factors determining demand?/Explain the factor affecting demand

- Price: – Price is one of the most important factors that affect demand. When the price rises demand falls and when the price falls demand rises.

- Income: – Income is directly related to demand. If consumer income rises demand also rises and if consumer incomes fall demand also falls.

- Size of population: – An increase in size population leads to an increase in market demand for goods and services.

- Taste, habits and preference: – A change in taste also changes the demand for a commodity. E.g. demand for past food has increased in recent years.

- Price of complementary: – if goods are jointly demanded like car and petrol when the price of a car rises, the demand for car and petrol both will fall.

- Advertisement: – Powerful advertisements create demand for the product. E.g. consumers buy new products like shampoos, and soap due to attractive advertisements.

- Weather condition: – Weather also affects demand. E.g. raincoats have demand only in the rainy season or more ice-creams in summer.

- Expectation about future prices: – If consumers expect a fall in the price of a commodity in the near future, they will demand less at the present price and vice versa. It shows that expectations about future prices affect demand.

- Taxation policy: – Government’s taxation policy affects demand. For e.g., a change in income tax will change consumers’ disposable income and therefore demand.

Q.3. Distinguish between:

Desire and demand.

| Desire | Demand |

| Desire refers to a feeling or a want for something. | ‘Demand’ refers to a desire for a commodity backed by the ability to pay and willingness to pay for it. |

| For Example Desire to own a luxurious sports car. | For example demand for Smartphone, Railway tickets, and Electric vehicles (EVs) |

| Desire may or may not be backed by financial power | Demand should be backed by financial power. |

| Desires are personal wants or preferences that may not consider economic factors, such as price or affordability. | Demand takes economic considerations into account. It factors in the willingness and ability to pay for a product or service at a specific price point. |

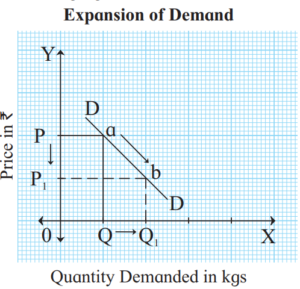

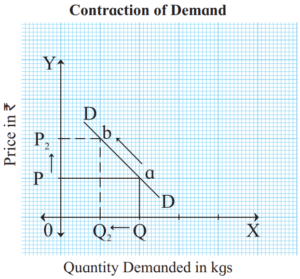

Expansion of Demand Contraction of Demand

| Expansion of Demand | Contraction of Demand |

| Demand of a commodity increases due to fall in price alone, other factors remaining constant. | Demand of a commodity decrease due to increase in price alone, other factor remaining constant. |

| When the price of a product decreases, consumers are willing and able to buy more of it. | When the price of a product increases, consumers are less willing or able to buy as much of it. |

| Extension of demand is often observed when there is a sale, price reduction, or promotional offer on a product. | Contraction of demand can happen when there is an increase in production costs, scarcity of resources, or when the product becomes less affordable for consumers. |

|

|

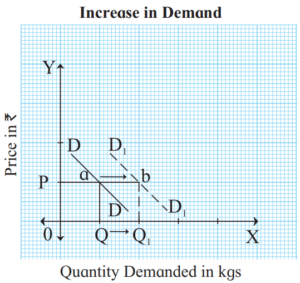

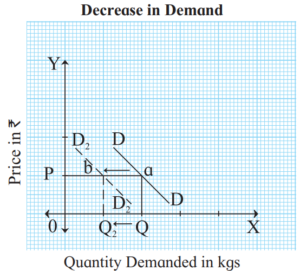

Increase in demand and Decrease in demand.

| Increase in Demand | Decrease in Demand |

| Increase in demand means a rise in demand due to changes in other factors, price remaining constant. | Decrease in demand means, a fall in demand due to changes in other factors, and price remaining constant. |

| The increase in demand can be caused by different factors such as an increase in consumer income, a change in consumer preferences or tastes, etc. | The decrease in demand can be caused by different factors such as a decrease in consumer income, a change in consumer preferences, availability of substitute products, etc. |

|

|

Define the Law of Demand, Explain its Assumptions and Exceptions

Introduction:-

- The law of demand was introduced by Prof. Alfred Marshall in his book, ‘Principles of Economics’, which was published in 1890.

- The law explains the functional relationship between price and quantity demanded. Generally, most people demand more when the price is less or falls and demand less when the price is higher or rises.

Statement of law:–

- According to Prof. Alfred Marshall, “Other things being equal, higher the price of a commodity, smaller is the quantity demanded and lower the price of a commodity, larger is the quantity demanded.”

- In simple words, the law of demand shows the functional relationship between price and quantity demanded.

- D = f (P), Where D = demand , P = Price F = function

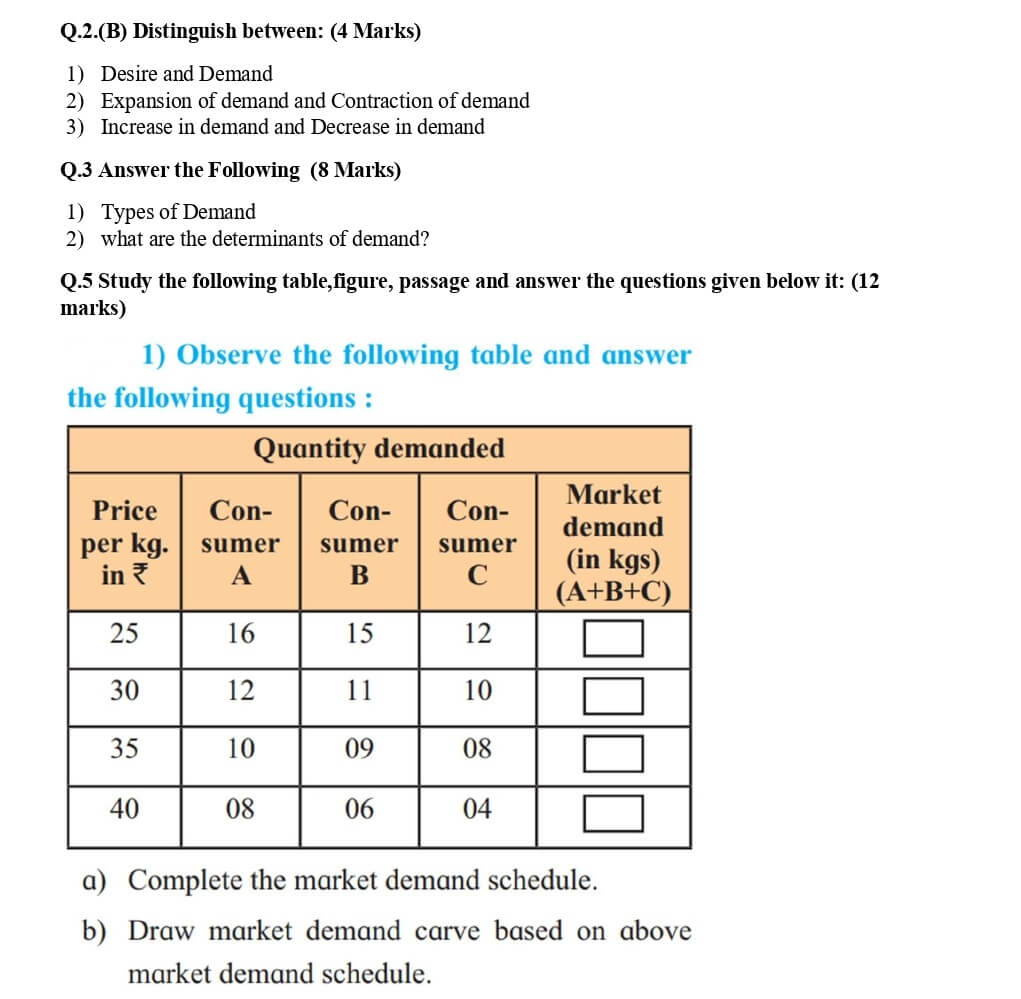

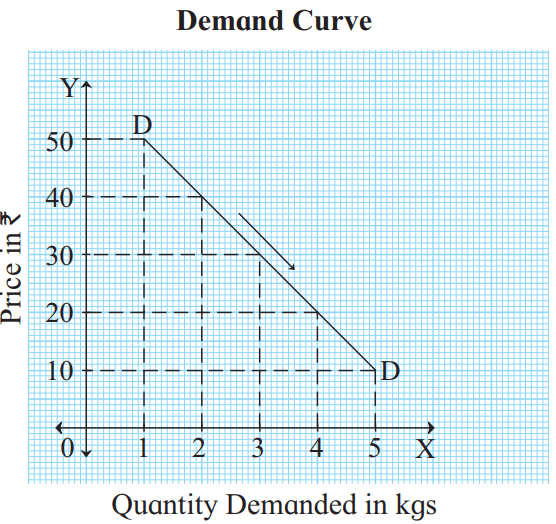

The Law of Demand can be explained with the help of the following demand schedule and demand curve.

Demand Schedule:

| Price per Kg. (Rs.) | Demand (Kg.) |

| 50 | 1 |

| 40 | 2 |

| 30 | 3 |

| 20 | 4 |

| 10 | 5 |

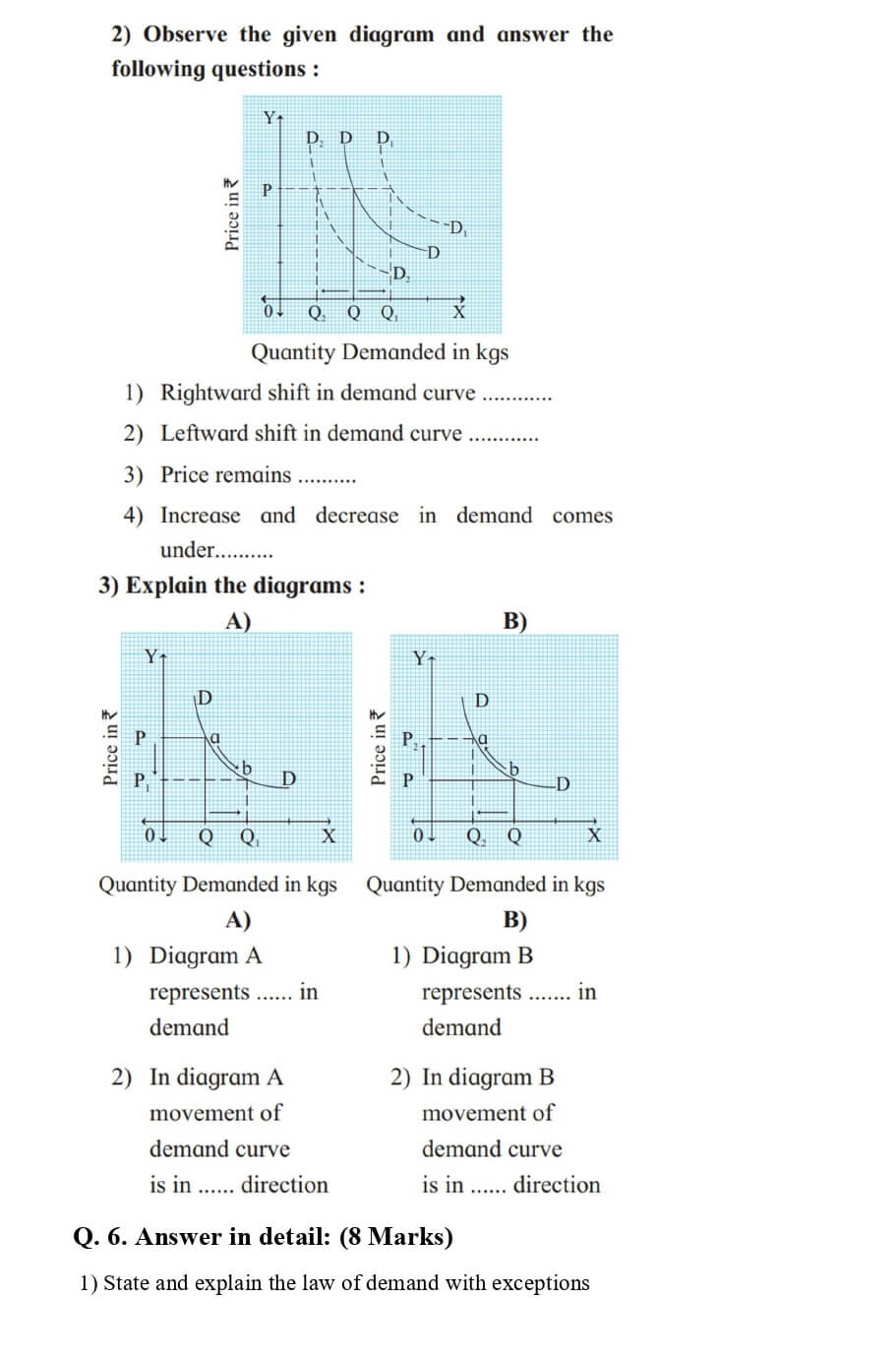

Demand curve:

Explanation of curve:-

- X-axis shows quantity of commodity demanded and Y-axis shows price of commodity.

- The demand curve slopes downwards from left to right.

- Demand curve shows the inverse relationship between price and quantity demand.

- This means that at higher the price less demanded and at lower price higher demanded.

Assumptions of Law of Demand

- No change in consumer income: – It assumes that there is no change in consumer income because if income increases consumers will demand more quantity even at a higher price.

- Size of population remains constant: – There should not be any change in the size of the population. Because a change in population will bring about a change in demand and vice versa.

- No change in the expectation of future price changes: – There not be any change in the expectations about the prices of goods in the future. If consumers expect that prices will rise or fall in the future, they will change their present demand through price is constant.

- No change in the price of substitute and complementary goods: – The price of substitute and complementary goods should remain the same. For e.g. if the price of tea rises, its demand will decrease but the demand for coffee will increase.

- Government policy remains constant: – No change in direct and indirect taxes imposed by the government. A change in income tax may cause changes in demand and vice-versa.

- No change in weather conditions: – Changes in weather conditions would affect the demand for certain goods, raincoats, woolen cloths, etc. So it assumed that weather conditions remain unchanged.

Exception of Law of demand:

- Giffen goods: – Inferior goods like bread, potatoes, etc. are those goods whose demand does not rise even if their price falls. Sir Robert in the 19th Century in England observed that when the price of inferior goods like bread fell, poor people purchased a small quantity of bread. This is because when their price fell, the real income of consumers increased and they brought more of some other commodities instead of demanding more of bread. This is known as Giffen’s paradox.

- Speculation: – When people speculate about rises in the price of goods in the future, they may buy more at the existing higher price. Likewise, when people speculate fall in the price of goods in the future; they will not buy more at the existing lower prices. They will wait for the price to fall in the future.

- Prestige goods: – Rich people buy costly things like diamonds, higher priced motor cars, and bungalows, etc. when their price is higher just to show off in society and vice-versa.

- Ignorance: – If the price of a product falls and if people are not aware of that, they do not buy more.

- Fashion: – if a commodity goes out of fashion, people do not buy more even if the price falls.

- Illusion: – With a fall in price, sometimes consumers feel that the product of quality is low and they do not want to buy more.

- Habitual goods: – Due to habitual consumption certain goods like tobacco, cigarettes etc. are purchased even if prices are rising. Thus it is an exception.

COMMENTS

Post your Comment

RECENT POST

How to Convert CGPA to Percentage in Mumbai University With Free Calculator

April 27, 2026

Maharashtra SSC & HSC Result 2026 – Date, Time & mahresult.nic.in Direct Link

April 25, 2026

11th Commerce Subjects & Free PDF Books – Maharashtra HSC Board 2026-27

April 23, 2026

Class 12 OCM important questions for HSC Maharashtra Board 2026

February 12, 2026Related Post

How to Convert CGPA to Percentage in Mumbai University With Free Calculator

April 27, 2026

Maharashtra SSC & HSC Result 2026 – Date, Time & mahresult.nic.in Direct Link

April 25, 2026

11th Commerce Subjects & Free PDF Books – Maharashtra HSC Board 2026-27

April 23, 2026

Your teaching is excellent I like the way u teach

sir you teach very well

Isa ka answer nhi. Mujhe chai hai