FEATURES OF PERFECT COMPETITION | FYBCOM BUSINESS ECONOMICS SEMESTER-2

FEATURES OF PERFECT COMPETITION

- Perfect competition is a market situation where a large number of sellers and large numbers of buyers buy and sell homogenous goods that are identical.

- In perfect competition seller is a price taker, sellers accept the price determined by the market demand and supply.

- There is no restriction for any person to produce and sell the existing commodity. Agricultural markets are commonly used as an example.

FEATURES OF PERFECT COMPETITION

- Large number of buyers and sellers: In perfect competition, there is a large number of buyers and sellers. The existence of a large number of buyers and sellers makes no influence on the price of the product. Therefore, the individual firm under perfect competition is a price taker because it does not influence the price. Firms have to accept prices determined by market demand and supply.

- Homogeneous or Similar products: It means that the product or commodity that is sold in perfect competition is similar or identical. when goods are homogenous there is no possibility of charging a higher price by any seller.

- Free entry and exit of the firm: There is no restriction for the entry and exit of the firm in the perfect competition market. Any producer to produce a commodity and sell it in the market freely.

- Complete market information: In perfect competition buyers and sellers have perfect knowledge or complete information about the market price, demand, supply, etc. Complete market knowledge helps buyers to pay higher prices.

- Perfect mobility of factors of production: Under perfect competition, the factors of production are assumed to be freely mobile. Factors of production such as labour and capital are assumed to be mobile. The mobility of factors helps the firm to adjust the market demand with the change in market supply.

- No transportation cost: It is assumed that there is no transportation cost under perfect competition. It applies when the production area and sales market take place in a small geographical area or the same area. For example, agricultural products are sold in the same village or town which requires no transportation cost.

Price determination under Perfect Competition:

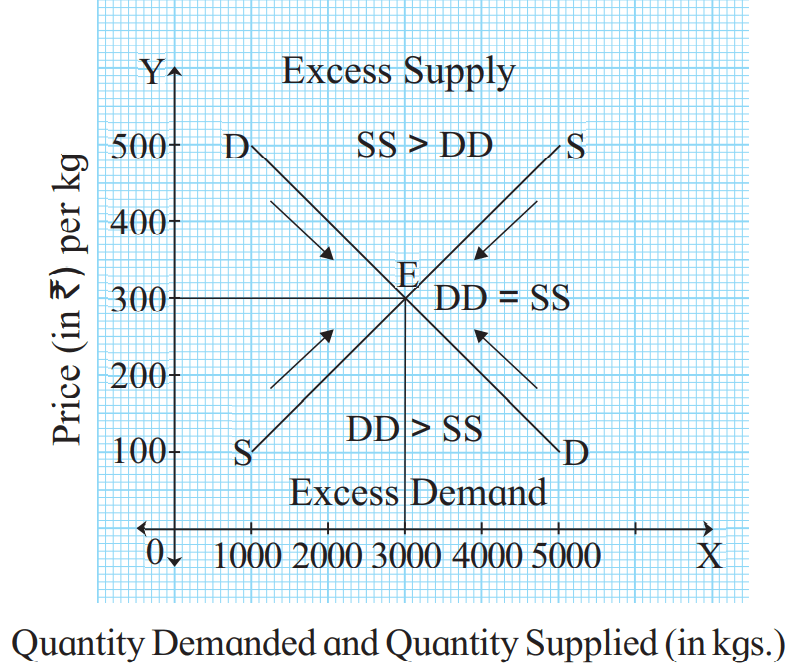

In perfect competition, price is determined by the interaction between demand and supply, A point where the demand curve cut the supply curve-determined price, and that is known as price equilibrium.

This is explained with the help of the following schedule and diagram.

| Price | Demand | Supply | Relationship between DD and SS |

| 100 | 5000 | 1000 | DD>SS |

| 200 | 4000 | 2000 | DD>SS |

| 300 | 3000 | 3000 | DD=SS |

| 400 | 2000 | 4000 | DD<SS |

| 500 | 1000 | 5000 | DD<SS |

When the price rises from ₹ 100 to ₹ 200 quantity demanded falls from 5000 kgs. to 4000 kgs. whereas supply increases from 1000 kgs. to 2000 kgs. This is because demand falls with a rise in price and supply rises with a price rise. This is the stage where demand is greater than supply (DD >SS).

When the price rises to ₹ 300, the quantity demanded and quantity supplied become equal that is 3000 kg. This is the stage of equilibrium where demand and supply become equal (DD = SS). Hence, ₹ 300 becomes the equilibrium price.

When the price further rises from ₹ 400 to ₹ 500, demand falls from 2000 kgs. to 1000 kgs. and supply rises from 4000 kgs. to 5000 kgs. Thus, supply is greater than demand. (SS > DD).

- In the above diagram, X axis indicates quantity demanded and quantity supplied, whereas Y-axis indicates the price. DD is the downward sloping demand curve which shows inverse relationship between price and quantity demanded. SS is the upward sloping

supply curve which shows direct relationship between price and quantity supplied. - E is the equilibrium point where DD and SS curve intersect each other. Accordingly ₹ 300 is the equilibrium price and 3000 kgs. is the equilibrium quantity demanded and supplied.

- This equilibrium price is determined by market demand and market supply.

SHORT-RUN EQUILIBRIUM OF A FIRM UNDER PERFECT COMPETITION

- Short run is the conceptual period where at least one factor of production is fixed in amount while other factors are variable

- The short-run is a period within which the firms can change their level of output only by increasing or decreasing the variable factors such as labour and raw material, while fixed factors like capital equipment, machinery, etc. remain unchanged or constant.

- A firm in the short run is in equilibrium at a point where Marginal Revenue (MR) is equal to Marginal Cost (MC) i.e. MR=MC and where MC is cutting MR from below

- The firm under perfect competition operates under the U – shaped cost curve. Since marginal revenue is the same as price or average revenue under perfect competition, the firm will equalize marginal cost with a price to attain the equilibrium level of output.

- A firm under perfect competition in the short run being in equilibrium does not necessarily earn profit. The firm determines the equilibrium level of output and price and tries to earn an excess profit or normal profit, or may even incur a loss.

Reference : Mumbai University

FYBCOM MCQ with Answers Click Here

For more Economics Notes Click Here

RECENT POST

How to Convert CGPA to Percentage in Mumbai University With Free Calculator

April 27, 2026

Maharashtra SSC & HSC Result 2026 – Date, Time & mahresult.nic.in Direct Link

April 25, 2026

11th Commerce Subjects & Free PDF Books – Maharashtra HSC Board 2026-27

April 23, 2026

Class 12 OCM important questions for HSC Maharashtra Board 2026

February 12, 2026Related Post

How to Convert CGPA to Percentage in Mumbai University With Free Calculator

April 27, 2026

Maharashtra SSC & HSC Result 2026 – Date, Time & mahresult.nic.in Direct Link

April 25, 2026

11th Commerce Subjects & Free PDF Books – Maharashtra HSC Board 2026-27

April 23, 2026